Critical supply chains are choked off. Demand soars. Prices surge and everyone starts freaking out about inflation and wonder how long it will last.

Is it 1945? 1916? 1974?

The answer, of course, is all of the above, and you can throw 2021 in there as well.

Inflation is not something new for the U.S. as the nation has weathered seven such episodes of lasting price surges since World War II including the current run, which is the strongest in 30 years. Getting out of the pandemic shock has been a difficult exercise for the world’s largest economy, and inflation has been a painful side effect.

But trying to find a historical parallel – and, thus, perhaps a way out – isn’t easy. Virtually every cycle bears at least some similarities to others, but each is unique in its own way.

The most common comparison to these days is the stagflation – low growth, high prices – environment of the 1970s and early ’80s. And while there’s probably at least some validity to that, the reality is more complicated.

“In terms of how widespread inflation is, it’s pretty much touching everything. It’s widespread, or more than what we saw in the 1970s,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group. “The question is, how long it remains elevated and when it backs off and at what rate does it settle out?”

Most U.S. policymakers reject the 1970s connection.

Leaders such as Federal Reserve Chairman Jerome Powell, Treasury Secretary Janet Yellen and Biden administration officials view inflation as temporary and almost wholly driven by factors unique to the pandemic. Once those factors subside, they see inflation drifting lower, eventually getting around the 2% level the Fed considers emblematic of a healthy and growing economy.

Some White House economists have asserted that the current stretch looks not like the stagflation era, but more like the immediate post-World War II climate, when price controls, supply problems and extraordinary demand fueled double-digit inflation gains that didn’t subside until the late 1940s.

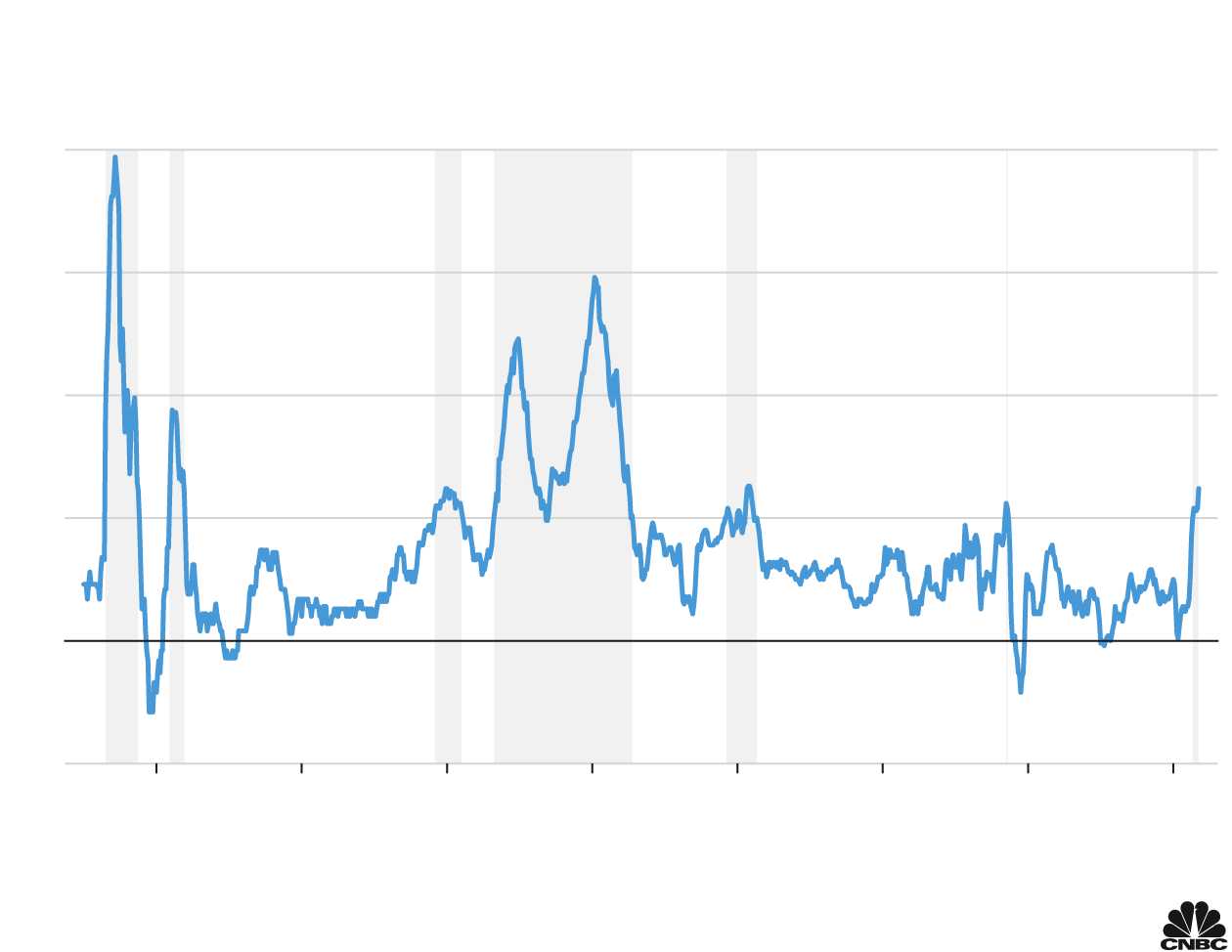

Episodes of U.S. inflation

Consumer price index, percent change from a year ago

20%

Post-WWII

Oil shocks

15

Korean War

10

Supply

Iraq invades

Late 1960’s

chain

Kuwait

Gas price

economic

disruptions

spike

expansion

5

0

−5

1950

’60

’70

’80

’90

’00

’10

’20

Note: Periods of heightened inflation are shaded.

Source: Bureau of Labor Statistics (CPI), White House (inflationary periods through ‘08). Data is

seasonally adjusted and as of Oct. ’21.

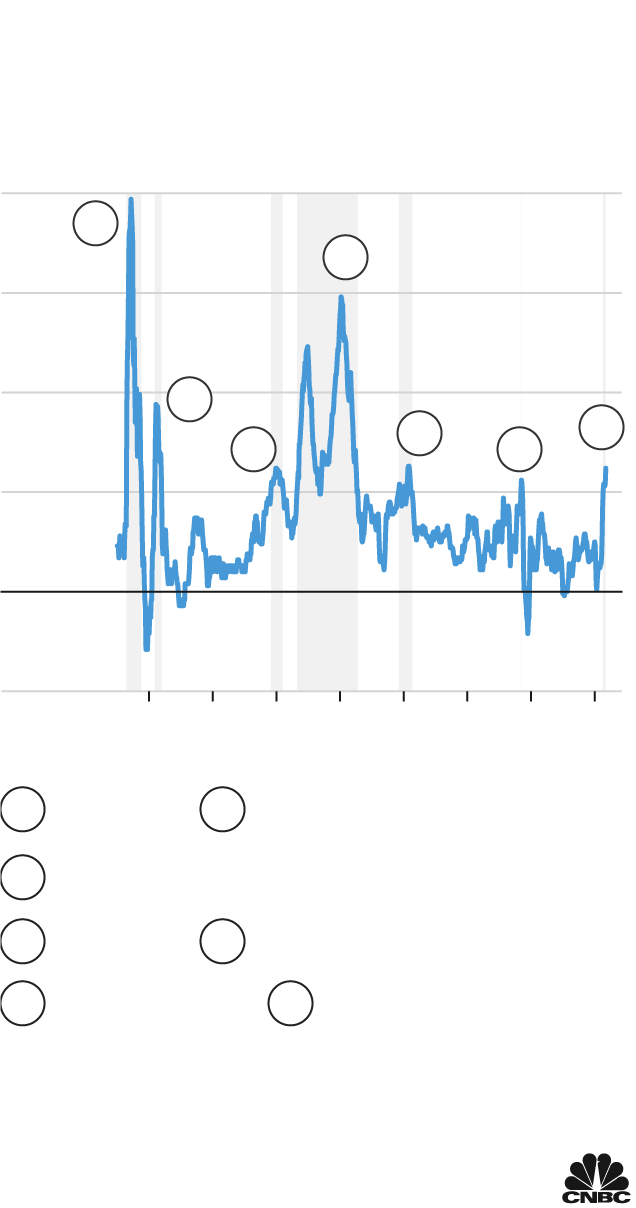

Episodes of U.S. inflation

Consumer price index, percent change from

a year ago

20%

1

4

15

10

2

7

5

3

6

5

0

−5

1960

’80

’00

’20

Post-WWII

Korean War

1

2

Late 1960’s economic expansion

3

Oil shocks

Iraq invades Kuwait

4

5

Gas price spike

Supply chain disruptions

6

7

Note: Periods of heightened inflation are shaded.

Source: Bureau of Labor Statistics (CPI), White

House (inflationary periods through ‘08).

Data is seasonally adjusted and as of Oct. ’21.

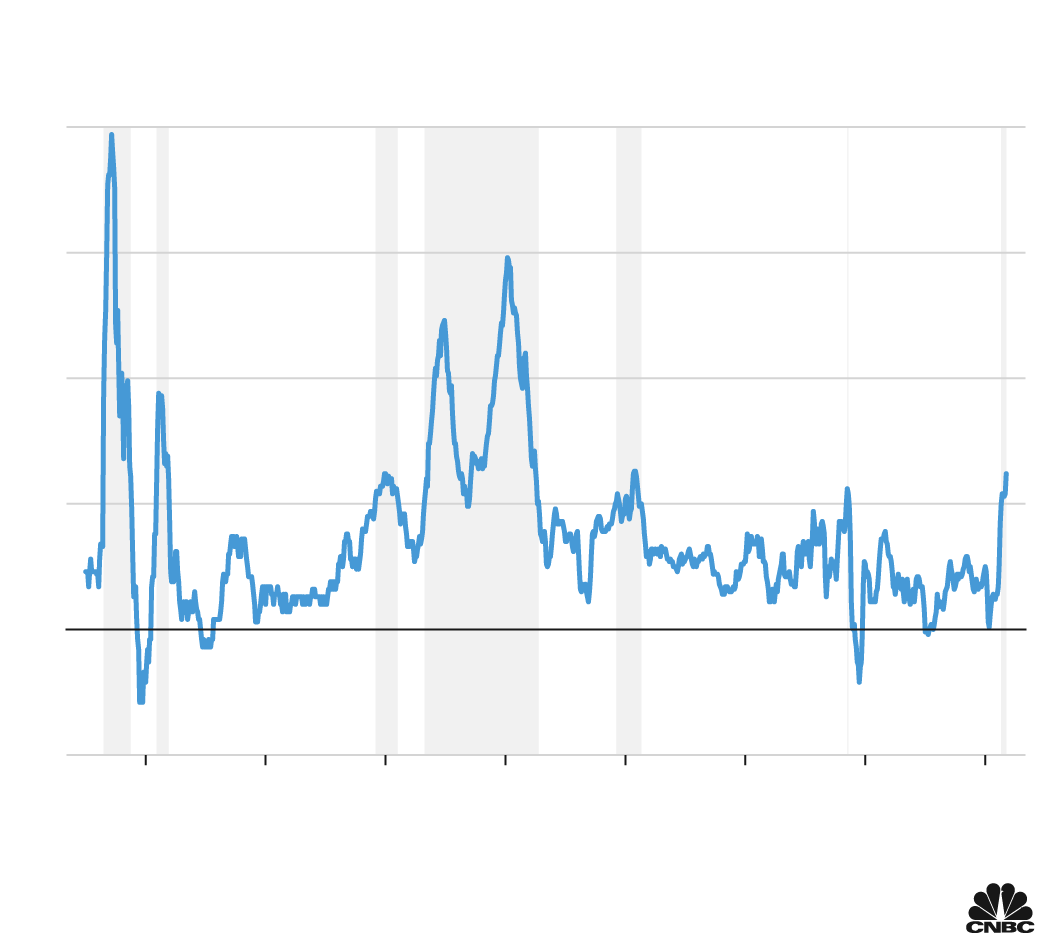

Episodes of U.S. inflation

Consumer price index, percent change from a year ago

20%

Post-

WWII

Oil shocks

15

Korean

War

10

Iraq

Supply

invades

Late

1960’s

chain

economic

Kuwait

Gas price

disrup-

tions

expansion

spike

5

0

−5

1950

’60

’70

’80

’90

’00

’10

’20

Note: Periods of heightened inflation are shaded.

Source: Bureau of Labor Statistics (CPI), White House (inflationary periods through

‘08). Data is seasonally adjusted and as of Oct. ’21.

“Today’s shortage of durable goods is similar — a national crisis necessitated disrupting normal production processes,” a team of White House economists wrote in a July 2021 paper. “Instead of redirecting resources to support a war effort, however, manufacturing capabilities were temporarily shut down or reduced to avoid COVID contagion.”

Once the supply chain disruptions are remedied – and there are signs that at least the major ports are becoming less crowded in recent days – “inflation could quickly decline once supply chains are fully online and pent-up demand levels off,” the paper stated.

Transitory, permanent or ‘in between’

The idea that inflation is “transitory” – a well-worn term that is transitioning out of vogue – is central to the insistence from fiscal and monetary authorities that excessively easy policy is not to blame for the inflation surge.

However, easy policy has been at the core of many previous cycles, and trying to blame everything on the pandemic hasn’t gone over especially well with consumers, whose confidence is running at decade lows, and on Wall Street, where investors are getting antsy over how long inflation will last.

Whether inflation is temporary, in fact, is probably the biggest debate happening in investing circles these days.

“The debate is always couched in black and white. The reality is, it’s probably in between there,” said Jim Paulsen, chief investment strategist at the Leuthold Group.

In fact, Paulsen has studied inflation over the past century or so and found that while there may been many periods where it has become problematic, there are only two where it proved lasting: after World War I and in the aforementioned 1970s-early ’80s.

He’s largely in the camp that this run, too, will pass as it has been fueled largely by supply chain problems that ultimately will resolve.

Still, he’s wary of being wrong.

“It’s not as temporary as we first thought, but I still think that’s the best odds” that it will pass in the coming months, Paulsen said. “But I’d also say that it is undoubtedly the biggest risk that it’s not. If it’s not, then it’s a disastrous outcome not only for stocks but also for the economy if it’s truly runaway.”

The inflation danger comes because this cycle is unlike any other in one important way: Policymakers have never thrown anything close to this amount of money at the economy.

What if sometime next year we not only declare pseudo-victory over Covid, but we declare it over inflation, too?Jim Paulsenchief investment strategist, the Leuthold Group

‘Abuse of policy’

While President Joe Biden and Yellen have insisted that all the fiscal and monetary stimulus is not the underlying cause of inflation, the argument that nearly $10 trillion between Congress and the Fed hasn’t pushed prices higher is hard to swallow for some.

Even though Paulsen believes the present conditions will fade in 2022, he worries about what he calls “global synchronized abuse of policy.” In essence, the meaning is that policymakers remain in emergency posture for an economic picture that seems long past crisis stage, with the potential for boiling over should officials continue to turn up the heat.

Still, he also sees declining commodity prices – with oil at the center – as well as falling shipping costs and the lessening of clogs at the ports as hopeful signs that inflation will, at least in historical terms, prove temporary.

“What if sometime next year we not only declare pseudo-victory over Covid, but we declare it over inflation, too?” Paulsen said.

The emergence of a new Covid variant in South Africa complicates both questions. Even Powell, Bush and others in the inflation-is-transitory camp say that the pandemic has been the root cause of price pressures, so if the new variant turns into a larger threat, that means inflation stays higher for longer.

Beside that, though, most mainstream economists are sticking to the belief that 2022 will say a significant drop in inflation.

How it all ends

Mark Zandi, the chief economist at Moody’s Analytics, feels that way even though he says there are close parallels between the current predicament and the runaway inflation of the 1970s.

For one, he said the waves in that inflation shock were both demand-driven and the product of supply issues because of the oil embargoes back then. Unions that were able to negotiate cost of living increases in contracts also boosted the wage-price spiral.

A sentient Fed also contributed to the problems by taking inflation too lightly and resisting the interest rate hikes that could have slowed the economy.

While Fed policymakers have been slow to tighten in the present day, they have vowed that if inflation expectations become unhinged, they’ll act. The worry, though, is that the Fed is already too late.

“The wage spiral that we suffered back then was because of the COLAs and the explosion if inflation expectations. They did rise and the Fed did not recognize that and did not respond to it,” Zandi said. “Assuming each future wave of the virus is less disruptive, then, yeah, I think we would see signs of moderation.”